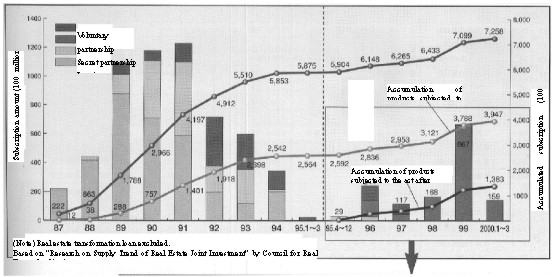

THE CURRENT STATUS OF JAPANESE REAL ESTATE MARKET - SECURITIZATION OF REAL ESTATEHogiko IWATA, JapanKey words: It has been a long time since 'the Japanese bubble economy burst'. Japanese land prices have continued been falling for the last ten years and real estate trade remains stagnant. To break this stagnation, much attention has been paid to the "securitization of real estate" as a way of "liquidation" of real estate. The related laws have been developed and gradually this system has brought some results. In the real estate and financial business, expectations are running high for developing a new real estate financial market (J-REIT). This time I would like to focus on the "securitization of real estate" in the current status of the Japanese real estate market. 1. HISTORY OF THE "SECURITIZATION OF REAL ESTATE" IN JAPANThe "securitization of real estate" is nothing new. It has been in the market as a product: "Mortgage backed security" based on the the Mortgage Certificate Law, which has been effective since August 1931 (the object of securitization is the right of pledge placed on real estate as collateral and securities issued by mortgage companies are circulated. They are not securities based on the Securities and Exchange Law) and small-lot commodities (sales and circulation of joint ownership of property rights, sales and circulation of trust beneficiary rights considering real estate to be fiduciary estate). However, mortgage backed security is a system which depends on the credit capability and guarantees in favor of the endorsement by mortgage companies. Unprincipled dealers are ousted by the law enacted in 1987. When the bubble burst, many small and medium sized companies went bankrupt and confidence in mortgage companies has dropped. This system is no longer popular among investors these days. Small-lot commodities were popular especially during the bubble economy. The first small-lot commodity of a trust type was real estate with lease cash flow of office buildings, which was divided into multiple property rights and sold to investors in March 1987. Its purpose was mainly the tax avoidance at that time, that is, with this commodity, even where operating profit after depreciation project is in the red, the loss can be offset and have advantages overall. Actually expectation for capital gain supported the system. In substance, small-lot commodities are the same as unsecured loans. Whether investors invest in small-lot commodities or not depends on the credit capability of selling organizations. In the first half of 1999, Tokyo Tatemono Co., Ltd. and Sumitomo Realty & Development Co., Ltd. could sell small-lot commodities because they had gained credit with an investors. Today small-lot commodities are on the wane due to their complexity and low marketability. In the past, an issuing organization with an unstable business foundation went bust and it became an object of public concern. The Real Estate Syndication Act, which requires issuing organizations with a license, was established to protect investors in 1995. Subscription Value of Real Estate Joint Investment Products

(Domestic Products) and Trend of Accumulated Value (Calendar Year)

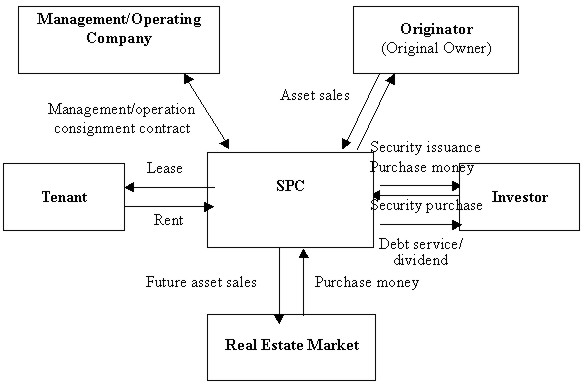

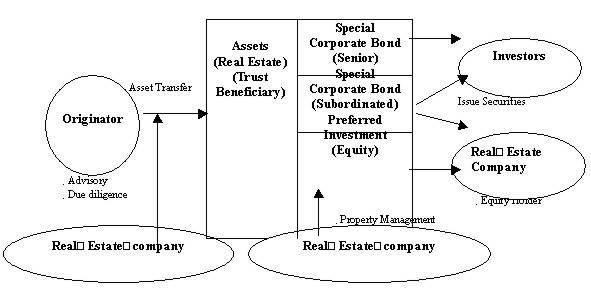

The securitization of real estate stems from the needs of both corporations and investors in the circumstances that real estate prices cannot be expected to soar after the bubble burst. Traditionally Japanese corporations have raised funds from financial institutions such as banks, backing their credit capability by the latent profits of their real estate. However, since their credit capability has been falling along with the drop in land values, each company has to seek new routes for fund procurement. On the other hand, investors have been searching new routes for investment due to low interest rates for a long time and declining stock prices. Then both needs match here and the securitization of real estate has been promoted rapidly. The SPC Law established in September 1998, which was originally reviewed as a part of the financial system revolution, was a trigger. Backed by the law called the SPC Law, the scheme of securitization and liquidation of real estate was realized by establishing a special purpose company (SPC) whose business is limited only to issuing securities backed by the specified real estate owned by the real estate owners (originators) and issuing corporate bonds and stocks by that SPC. The performances of SPC based on this SPC Law are shown in Exhibit 1. 2. SECURITIZATION OF REAL ESTATE THROUGH SPCThe fundamental structure of the securitization of real estate by SPC is the structure to raise funds directly from investors by issuing securities such as corporate bonds and stocks backed by cash flow (income of rent and capital gains etc.) which is generated by the assets which are transferred to SPC from an originator in order to separate from other assets. SPCs exist only for issuing securities and are dissolved by disposal of the real estate. The basic scheme is as follows:

The significance of securitization by SPC The significance of securitization by SPC contains as following:

Since the SPC Law defines the protection for investors and disclosure rule, it becomes easier for general investors to enter the real estate investment market. Real estate investment used to be exclusive and complicated. Since securitization increases transparency of investment and investment funds can be collected from both inside and outside Japan, the real estate trade is expected to be vitalized in the long run. Here are merits of originators and investors. Originators' Merits

Investors' Merits

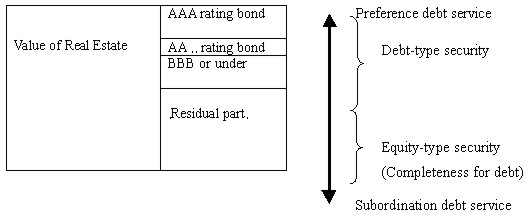

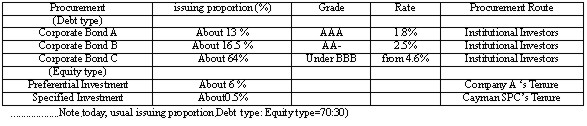

Securities Structure Real estate securities can be broadly divided into two categories: Debt type securities such as corporate bonds and equity type securities which are fund certificate type. Debt type securities utilize cash flow generated by real estate as the reversion source of revenue and they define its term, interest, and redemption amount. In debt type securities, a senior and subordinate structure is often created. On the other hand, equity type securities are the participation right to profits after interest payment, redemption, and repayment of debt. Therefore, for debt investors, equity part means credit enhancement and also high risk and high return because equity part condenses risks. (There are leverage effects.) Structure of senior and Subordinate Securitization

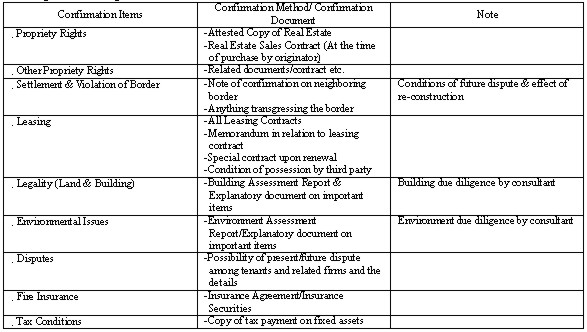

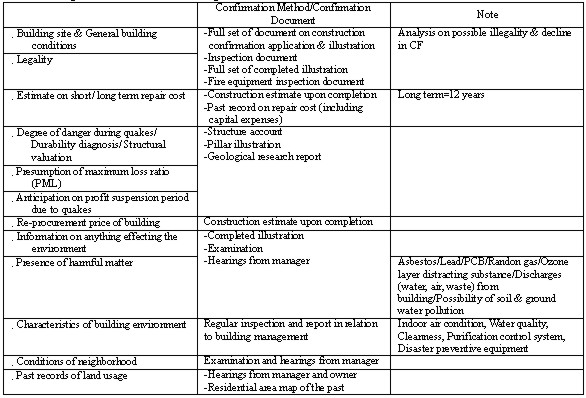

Independent specialized organization in securitization structure Real estate includes different risks from other financial assets: geology and soil risks, regional economy risks for rise and fall of the region, physical deterioration of buildings and facilities, and obsolescence due to deepening economic and social needs. Therefore, long-term cash flow of real estate depends in a large measure upon the initial condition of the property related to the business project (such as conditions of site, construction and maintenance conditions, use application) and management and administrative skills. That is the reason, why securitization needs specialized organizations for due diligence, project management of real estate development, assets management, property management etc. There are business opportunities for real estate corporations and investigating corporations here. Due diligence In order to disclose expected earnings and risks of the related real estate to investors, the purpose of due diligence is to measure and evaluate the total value as correctly as possible. In securitization, arrangers instead of investors acquire objective evaluation statement from independent specialized organizations. Specific due diligence elements are as follows: 1. Legal Due Diligence

2. Building/Environment Due Diligence

3. Accounting Due Diligence

The scheme in the case where real estate companies are involved in real estate management

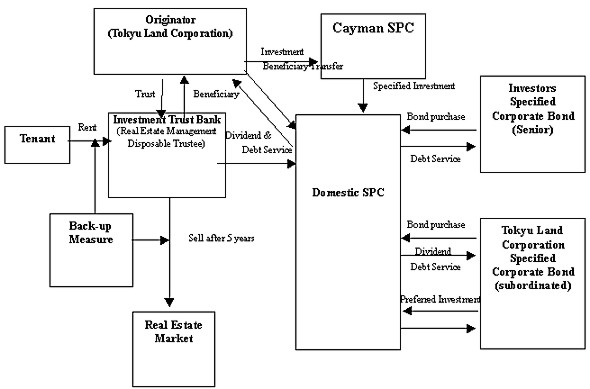

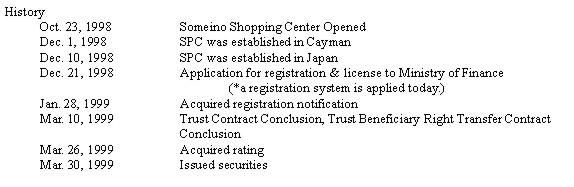

Case study Property Overview

Securitization features

Structure Overview

Issued Securities Overview

SPCs based on the SPC Law have many regulations and complicated procedures. Even after establishment of the SPC Law, the SPCs not depending on the SPC Law have often been utilized. In May 2000, the SPC Law was amended and the scheme has become easier to be utilized. 3. THE SCOPE OF REAL ESTATE SECURITIZATIONSince the SPC Law came into force in September 1998, a lot of real estate securitization has been seen. Debt parts, once acquire rating, along with Asset Backed Securities (ABS) such as credit receivables, lease receivables, are considered to be profitable investments for institutional investors. In the short term, they have penetrated the market. However, as for equity parts, the needs of originators who do not want to release control of real estate and investors who are trying to obtain high-risk equities are quite limited. Therefore, originators often obtain equity parts. In May 2000, accounting principles on off-balance sheet became clear and the ceiling of ownership ratio was made. More equity parts will be expected to be on the market down the line. According to asset backed of ABS issued in the first half of 2000 and in 1999, real estate-related assets account for very large portion. In 1994, 'the ban on ABS' was withdrawn and the amount issued has been rapidly increasing. However, the amount of ABS issued in Japan in the first half of this year (public offering) tumbled about 11% from a year earlier to 505.6 billion yen. This is the first time a decline has been seen since the ban was lifted, while the amount of commercial mortgage backed securities (CMBS) and ABS issued whose assets are backed by housing loans has increased steeply (from 16.9% to 52%). This was because of consecutive securitization of large-scaled property in the distribution industry such as department stores and major supermarkets. J-ReitAmendment of the Securities Invest Trust Law in May 2000 made investment trust on real estate possible in Japan. Securitization by SPC is a company-type and trust-type scheme which collect investment money issuing the ABS(to investors) by cash flow and assets value of specified real estate. Investments trust is an asset-management-type scheme which produces income through investing the funds collected from investors (by issuing negotiable securities etc.) on real estate and real estate financial products, and divides the income to investors. In the case of corporate type investment trusts, the securities issued by the investing corporation become liquid as the corporation goes public and retail investors dealing with high risk and high return equities are expected to appear. Today, major Japanese real estate companies are preparing for establishing investment corporations and listing on the Tokyo Stock Exchange. For example, by April, Mitsubishi Estate Co., Ltd. will establish a 100 billion yen fund (an investment corporation) and it will be listed as the first Japanese real estate investment trust. It will deal with only good risks with more than 90% of capacity usage ratio such as office buildings in Marunouchi and 3-5 % dividend yields per year will be expected. Mitsui Real Estate Co., Ltd. will also establish large-scale fund (about 200 billion yen) by the end of June. Since the bubble burst, the Japanese real estate market has been groaning under no new inflow of fund and price slump. Our hopes rest on the degree to which J-REIT will attract into the real estate market the funds of the small-scale segment of the 1,300 trillion yen individual financial investor sector. BIOGRAPHICAL NOTEHogiko Iwata is a Licensed Real Estate Appraiser and a member of the Japanese Association of Real Estate. He was born in Gifu, Japan and has studied law at Hitotsubashi University Tokyo, where he graduated in 1980,working as the real estate appraiser since 1988. He is currently Manager of the Asset Management Department of Tokyo Land Corporation. CONTACTHogiko Iwata 30 April 2001 This page is maintained by the FIG Office. Last revised on 15-03-16. |